The figures

- 39.84 billion euros: the CA 2024 textiles, stable vs 2023

- +0.3%: volume evolution, at 2.6 rds of items

Source: Kantar, Total 2024 clothing, shoes, accessories and linen

The various panels of the Commerce Alliance, the French Institute of Fashion (IFM) and Kantar show that the clothing market stabilized in 2024. According to the trade alliance, sales were particularly “dependent weather” in 2024, consumers having shunned the summer collections with rainy spring while the arrival of cold in September encouraged them to buy large parts. An observation shared by Hélène Janicaud, fashion expert at Kantar : “If the expenses remained stable compared to 2023, we observe a very slight dynamic in volume (+ 0.3 %) fired by the start of the school year. The end of the year was calmer. »»

Other good news: the frequency of purchase “Is slightly over 1 %. It is important enough to be notified with regard to the continuous decline that we had since 2019continues Hélène Janicaud. However, we will have to compose with a market that has been reduced. Consumers do much less pulse purchases. They reflect their expenses and buy when they need it. »» Despite the slowdown in inflation, consumption has not frankly left. If the prices of clothing items have increased by 0.5 % on average last year according to IFM, they have nevertheless climbed by 10 % since 2021.

Consumers are particularly focused on prices, which promotes large dissemination chains and penalizes premium. According to the IFM, the majority of the circuits selling textiles have not found their levels before Covid: the turnover generated last year remain an average of 5.5 % lower than those of 2019.

Only the pure players and the wide diffusion channels of the Kiabi type, the Halle and Primark saw their sales exceed their level of 2019. “I do not think that the market will regain its level of then, 2019 will probably remain a peak in consumption for the market as had been 2007”advance Gildas Minvielle, director of the IFM Economic Observatory.

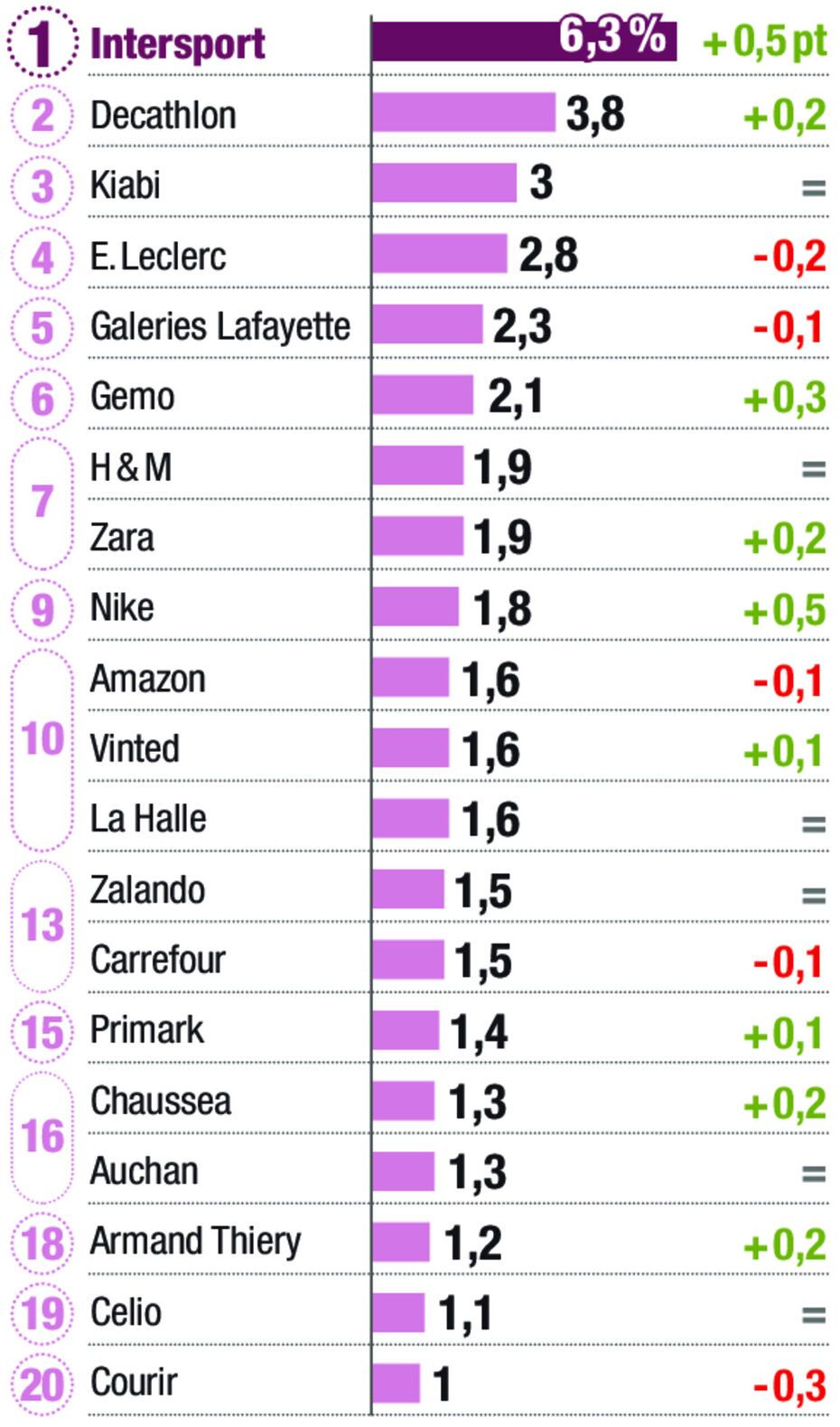

Intersport digs the gap

Top 20 fashion players according to their market share in value, in %, and evolution over one year, in PT

Source: Kantar, Total 2024 clothing, shoes, accessories and linen

Intersport and Decathlon comfort their leader’s place. Vinted climbed up to Amazon.

GSA loss of speed

On the circuit side, large food surfaces (GSA) accuse the strongest decline. Over the years with the appearance of fast-fashionnew balances as action and now the meteoric growth of ultra fast-fashion Shein type, the GSAs have lost ground on the low prices segment. Many brands have reduced their textile offer in stores, which does not make the radius attractive.

« Thirty years ago, the market share of hypermarkets and supermarkets was 17 %. Today, it is less than 10 % ”notes Gildas Minvielle. Indeed, according to Kantar, their market share was 7.7 % in 2024, compared to 8.3 % in 2023. Conversely, sports brands and periphery channels increased and gradually come closer to downtown and shopping center chains, market leaders.

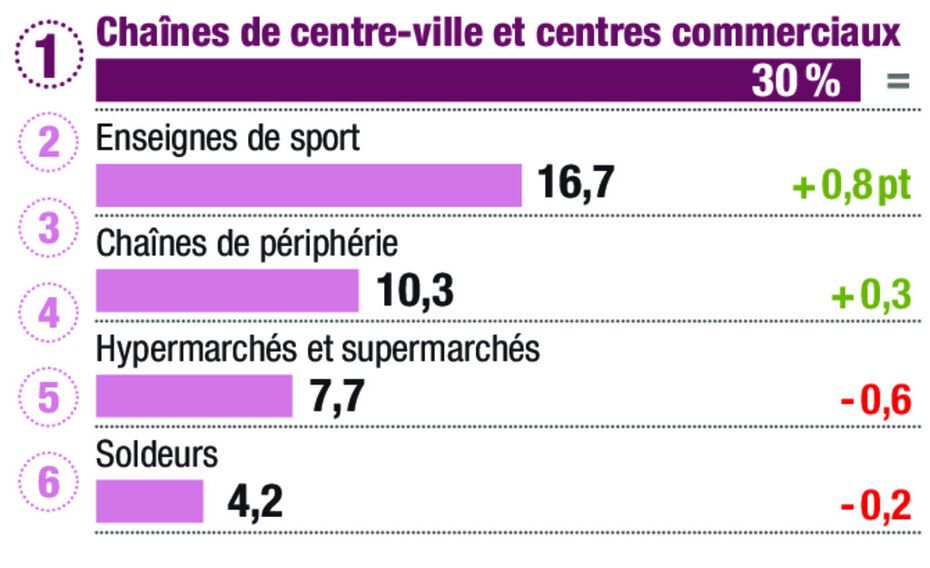

Downtown chains and shopping centers still leaders

Top 5 distribution circuits according to their market share in value, in %, and evolution over one year, in PT

Source: Kantar, Total 2024 clothing, shoes, accessories and linen

Sports brands and periphery channels continue to rise, while GSAs continue to drop.

The enthusiasm for sportswear brands does not weaken and this benefits Intersport, the first seller of national brands, which confirms its place as a leader in value. This also benefits Nike, the market share of which increased by 0.5 points (like that of Intersport), the strongest increase among the first 20 players in the fashion market.

Digital rise

Another strong trend: the rise of digital. E-commerce sales earned 1.8 %, while store sales lost 0.5 %. « There are fewer customers in stores than before, notes Hélène Janicaud. There is a real issue to make them come back. »» Online sales represent 21.8 % of the market, estimates Kantar. Chinese platforms offering ultra fast-fashion participate in this dynamism. “All brands combined, Temu has progressed the most in number of transactions”underlines Hélène Janicaud.

Also note the market share of Vinted, which with its 23 million users in France, is now equivalent to that of Amazon. Beyond Vinted, the entire second-hand market is gaining ground. “While the new market fell 0.6 % in value and 0.5 % in volume, the occasion increased by 6.5 % in value and from 7.6 % in volume, representing 4 to 5 % of the market last year “, Details Hélène Janicaud. A rise in power which should continue in the years to come with the development of the offer. According to IFM, in 2024, 58 % of brands-stage offered second-hand products, ten points more than in 2023.

In mid-March, Kantar was tabling for a resumption of expenses this year and estimated that the textile market would return the 40 billion euros mark with growth of 1.8 %. But that was without counting on Donald Trump’s announcements about American customs duties … Announcements that have destabilized the global economy and created an anxiety -provoking climate in favor of consumption.

{kind=link}