The reactions in Asia and North America suggest seemingly very different perceptions of the project to acquire the Japanese conglomerate Seven & I by layer-tard diet.

Posted at 7:00 a.m.

Investors could react Thursday to Seven & I’s decision to give Couche-Tard better access to his books, an important step to advance talks, and the behavior of investors is reflected.

The action of the operator of convenience stores 7 – Eleven won 2 % in Tokyo, which seems little compared to the progress which seems to have been made with the signing of a confidentiality agreement, comments analyst Martin Landry, of the Firm Stifel.

Seven & I’s action continues to negotiate an discount of almost 20 % compared to the revised offer of Colat-Tard, valued at 47 billion US.

This discount demonstrates all the ambient skepticism in the face of the realization of a transaction.

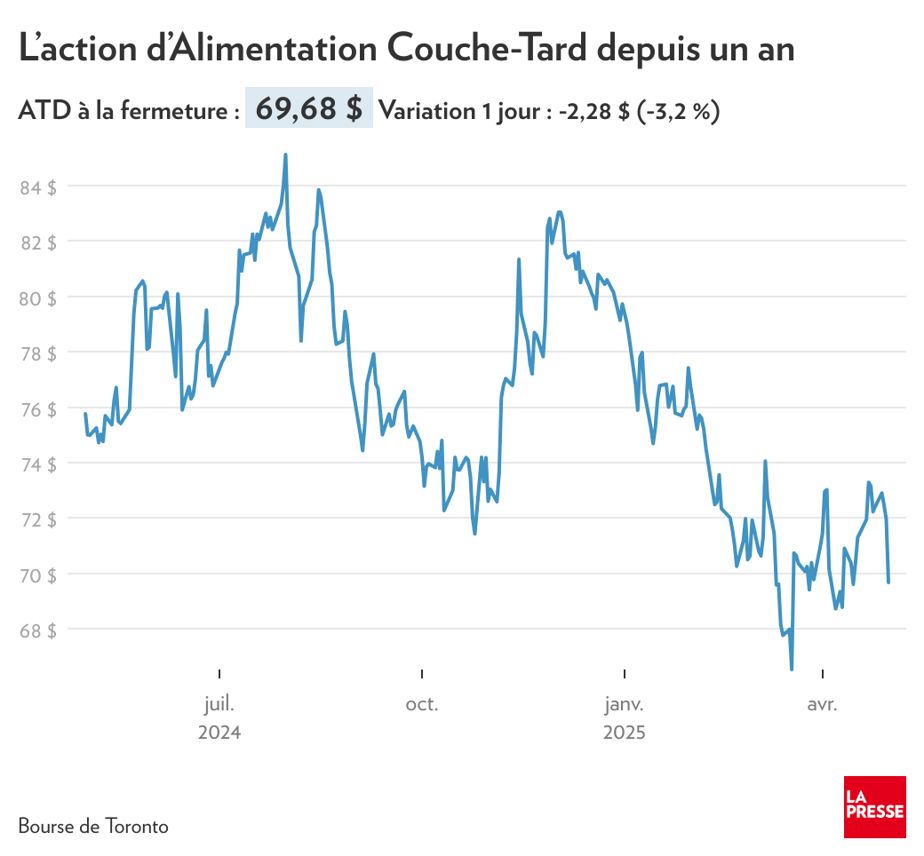

On the other hand, the action of Couche-Tard fell 3 % on Thursday in Toronto.

Some investors hesitate

This decline is notably a reflection of the fears of investors in connection with the size of the transaction envisaged, according to Martin Landry. “It’s huge,” he says.

Investors would apprehend the risk associated with the operation for what it would add to the debt-tard debt level, as well as the risk of dilution.

Some investors would be hesitant to buy or have the Action of Couche-Tard before a potential program of shares related to a transaction.

-Martin Landry is not very surprised by the weakness of the title of Lord-Tard observed during the Thursday session.

Whenever it has appeared that the negotiations were progressing between ATTARD and Seven & I in the last months and that the probabilities surrounding a transaction seemed more favorable, the title of ADTARD TARD, he said.

Conversely, whenever obstacles appeared suggesting that the chances of attending a transaction decreased, the title of a knockdow was appreciated, he underlines.

For his colleague Irene Nattel, at RBC, the signing of a confidentiality agreement is a step in the right direction for Coit-Tard, but the road to be done is still very long.

It is far from certain that an agreement will be concluded and approved by the regulatory authorities

Irene Nattel, at RBC, in a note sent to its customers on Wednesday

The management of Couche-Tard notably said that the privacy agreement aims in particular to help work in collaboration within the framework of possible dialogues with the regulatory authorities.

The development announced on Wednesday evening comes just a few weeks from the holding of the Japanese conglomerate shareholders’ assembly scheduled for May 27.

Behind the scenes, it is whispered that Seven & I’s decision to give Couche-Tard a better access to his financial data could be only a smoke screen to appease tensions before the shareholders’ assembly.

Doubts remain as to the will of the management of Seven & I to sell in Couche-Tard and the timid stock market reaction observed in Tokyo on the action of Seven & I could partly reflect these doubts.

{kind=link}