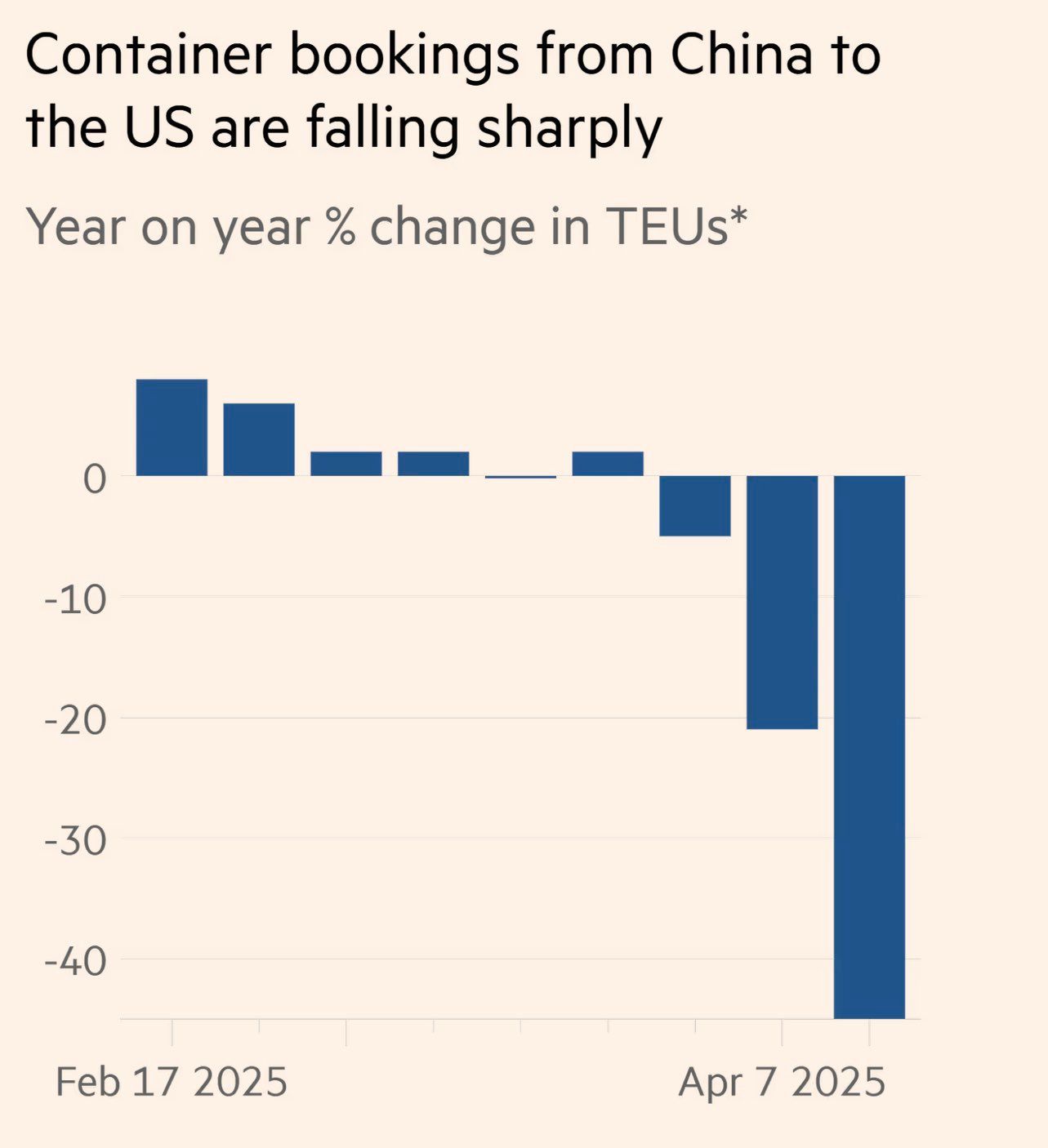

The week’s graph shows a spectacular drop in container reservations from China for the United States between February and April 2025, with a collapse of more than 40% in annual sliding on April 7. This brutal dropout illustrates a massive slowdown in trade between the two countries, a likely consequence of the rise in power of American protectionist measures, in particular increases in customs duties.

According to Freight Waves, the global volumes of container reservations fell 49% between the last week of March and the first of April 2025. Imports from China to the United States dived by 64%, while those of clothing and textiles fell 59% and 57% respectively, exceeding the crisis levels observed during the Pandemic of Cavid-19.

This spectacular decline reflects a generalized blocking of the global commercial channel: neither American importers nor Chinese exporters want to absorb the costs of new prices. The result is a wave of order cancellations, the accumulation of unsold containers in the Chinese ports, and a global overcapacity of global production much higher than forecasts.

Contrary to popular belief that the American consumer pays most of the invoice, the data indicate a much more elastic demand than expected: buyers simply refuse to pay more. This dynamic jeopardizes hundreds of exporters – especially in China – who find themselves exposed to a risk of bankruptcy for lack of sufficient working capital.

Faced with this brutal imbalance, two scenarios are emerging: either an acceleration of commercial negotiations, or the risk of a global recession, even a depression for economies strongly dependent on exports. In Europe, concerns also grow in the face of a possible influx of low -cost Chinese products, diverted from the American market, which could weaken local producers.

On the ground, trade tensions are starting to affect the real economy concretely, especially in the goods transport sector in the United States, where the slowdown increases: in one month, the volumes of road freight fell 8.3%, reaching levels comparable to those of the hollow of the Cavid crisis.

In some industrial states such as Michigan, truck drivers have not been charged for more than two weeks, especially in the automotive sector (GM, Ford). This sudden contraction of logistics activity fuels a wave of stress in the banking sector linked to the non-reimbursement of lease credits on truck fleets, some have not been honored for more than a year.

However, several financial analysts believe that rapid regulations for the current trade war-initiated around Valentine’s Day with the announcement of new customs tariffs-would avoid a collapse comparable to that of 2020. On the other hand, if the pricing show between the United States and China was to settle in the duration, the consequences could extend to the whole North American industrial fabric, with the key structural economic, orders of orders, bankruptcies in transport and a contraction of employment in the manufacturing sectors.

Beyond the raw data, this figure highlights the ideological fractures that today cross the United States. For supporters of a nationalist economy, this fall constitutes a strategic success: it demonstrates the decline in imports from China, the emergence of industrial autonomy, and, ultimately, increased consumption of local products by the Americans.

Conversely, other observers see it as the alarming sign of an increased risk of shortages, imported inflation and logistical disturbances, in particular in large distribution and within the supply chains.

In short, the same alarm curve or reassures according to everyone’s political reading grid: for some, it embodies an inflationary shock and economic derailment; For the others, a sovereignist success and a salutary break with China. This polarization reveals how interpreted economic facts are interpreted through antagonistic accounts, making any objective reading more difficult to make.

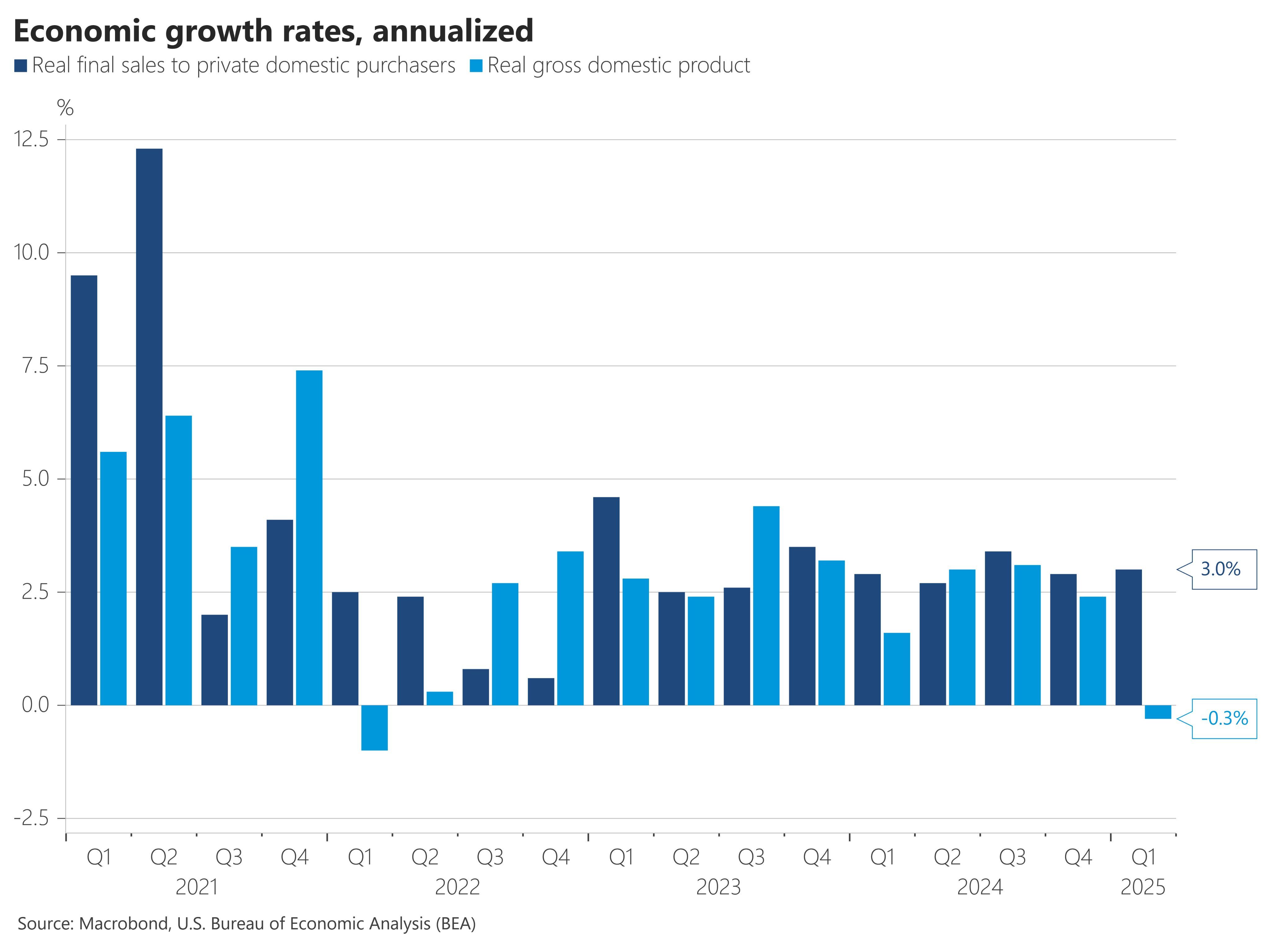

This divergence of interpretation is also manifested in reading the recent contraction of American GDP. For opponents of Donald Trump, this decline marks the entry of the country into recession, directly caused by tariff climbing. His supporters, on the other hand, mainly see the effects of the so -called “Doge” fiscal policy, focused on reducing public spending – which, mechanically, weighs on GDP. In other words, according to them, the level of growth under Biden would have been artificially inflated by excessive public demand.

Supporters of the current president highlight encouraging indicators, starting with the solidity of retail:

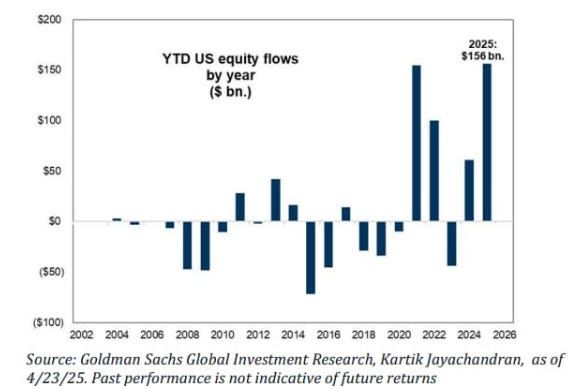

Inflation displays signs of lull, and the financial markets have significantly rebounded, carried by a record influx of new investors:

But the most skeptical nuance this reading: according to them, the vigor of retail sales would be explained above all by an early storage phenomenon with a view to the entry into force of new customs duties. Likewise, the massive return of private investors (Retail) would be typical of the deceptive rebound phases in a lower market.

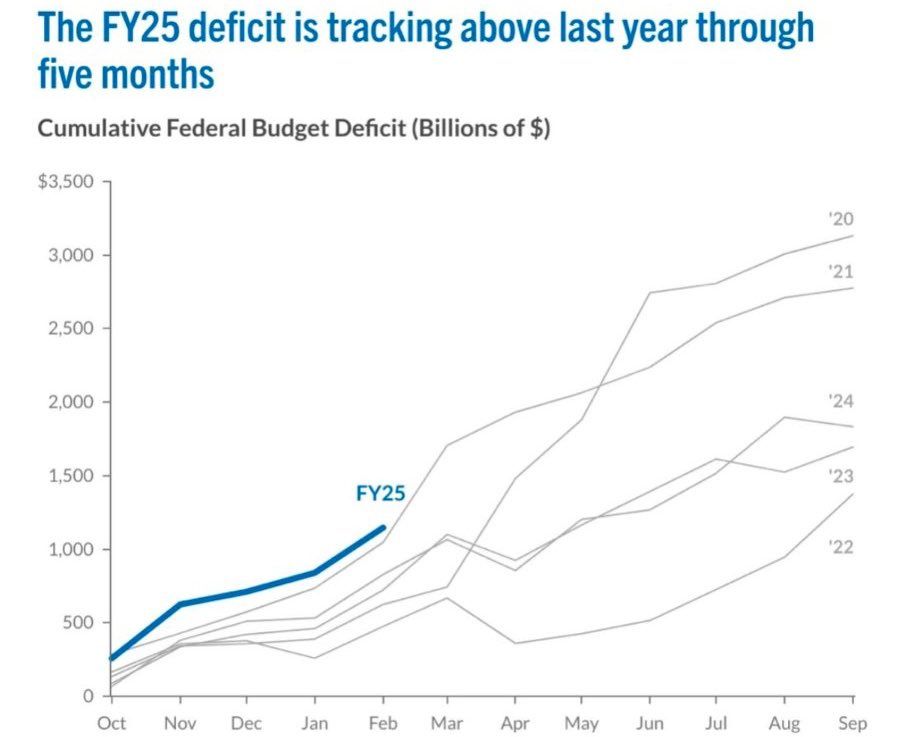

While the debates rage in the United States on the future trajectory of the economy and markets, a fact remains unchanged since the change of administration: the continuous progression of the budget deficit remains a major source of concern. On this front, no improvement is in sight; On the contrary, the situation deteriorates. This is a logical consequence: the load of public debt explodes in an environment where interest rates remain at unbearable levels for such a level of deficit.

It is precisely this disturbing trajectory of public debt that gold seems to continue to follow closely, which partly contributes to explaining its current outbreak.

Reproduction, integral or partial, is authorized provided that it contains all hypertext links and a link to the original source.

The information contained in this article has a purely informative nature and in no way constitute an investment council or a recommendation for purchase or sale.

--

{kind=link}